Growth Planning and Financing: How to Fund Your Next Stage Without Losing Control

Every business reaches a point where the next stage of growth requires more than ambition. Whether that's expanding operations, entering new markets, acquiring a competitor, or building out the team, growth requires capital. And how you fund that growth determines as much about the outcome as the growth initiative itself.

This post is about how to think about growth financing clearly to match the right capital to the right purpose, and to build a plan that funds your ambition.

The Two Mistakes Growing Businesses Make

Before getting into how to fund growth well, it's worth naming the two most common mistakes.

Mistake 1: Funding growth with the wrong type of capital

Not all capital is equal. Debt, equity, and internal cash flow each have different costs, different implications for control, and different appropriate uses. Funding long-term growth investments with short-term debt or giving away equity to solve what is really a cash flow timing problem, can both be expensive mistakes.

Mistake 2: Thinking about financing after the growth decision has been made

The sequence matters. Most business owners decide what they want to do and then go looking for the money to do it. The businesses that fund growth most effectively do it the other way around: they understand their financing options before they commit to the plan, which allows them to structure the growth initiative in a way that maximizes their financial flexibility.

The Four Sources of Growth Capital

1. Internal cash flow —> the most underrated source

For many growing businesses, the most powerful source of growth capital is the one they already have: the cash their business generates.

The challenge is that internally generated cash is often absorbed by working capital by being tied up in receivables, inventory, and the timing gaps between spending money and collecting it. A business that looks profitable on paper can have very little free cash to deploy toward growth.

Unlocking internal capital starts with financial discipline: tightening your cash conversion cycle, managing working capital actively, and building a cash flow forecast that shows you when capital will be available and when it won't.

In a high-rate environment, this source of capital becomes even more attractive. It costs nothing, requires no dilution, and keeps you in full control.

2. Debt —> powerful when used correctly

Debt is the most common external source of growth capital for SMEs, and in the right circumstances it remains compelling even at current rates because the cost of debt is known, fixed (in many cases), and tax-deductible, while the upside of the growth it funds is entirely yours (after the debt servicing payments).

The key is matching the type of debt to the purpose of the capital:

Term loans: best for defined capital investments with a clear payback period (equipment, fit-out, acquisition)

Revolving credit facilities: best for working capital needs that fluctuate with revenue

Asset-based lending: best where the business has strong receivables or inventory that can be used as security

Private credit and structured financing: best for more complex situations where bank debt doesn't fit, or where speed and flexibility matter more than rate

In the current environment, with rates elevated and banks more selective, private credit has become an increasingly important tool for growth-stage businesses that need capital quickly or have a story that a bank's credit committee struggles to underwrite.

3. Equity —> the most expensive capital, often misunderstood

Equity is often thought of as "free" capital because there's no interest to pay. It isn't free; it's the most expensive capital available because it costs you a share of everything your business earns, forever.

That doesn't mean equity is wrong. For businesses with high capital needs, long payback periods, or genuine uncertainty about future cash flows, bringing in an equity partner can be the right answer. Private equity, family offices, and strategic investors all have a role in the growth financing landscape.

But equity should be a choice and not just a default when debt feels too expensive or hard to access. Giving away 20% of your business to solve a problem that a well-structured debt facility could have addressed is a decision that compounds over time.

4. Vendor and creative financing —> often overlooked

Some of the best growth financing doesn't show up in a term sheet. Extended supplier terms that improve your cash conversion cycle. Earnout structures in acquisitions that reduce the upfront capital requirement. Revenue-based financing for businesses with strong recurring revenue. Customer deposits or advance payments that fund production before the invoice is raised.

These structures won't fund every growth initiative. But for the right situation, they can meaningfully reduce the external capital required and preserve both cash and equity for higher-priority uses.

How to Think About Capital Structure

The most important concept in growth financing is capital structure: the balance between debt and equity in your business, and how that balance affects your cost of capital, your financial flexibility, and your ability to execute on your strategy.

A business with too much debt relative to its earnings is fragile since a revenue shortfall or an unexpected cost can quickly become a crisis. A business with too little debt is leaving value on the table, using expensive equity to fund things that debt could have funded more cheaply.

Finding the right balance and maintaining it as the business grows is one of the most valuable things a strong finance function provides. It requires understanding your business's cash flow characteristics, your risk tolerance, the cost of different capital sources, and the likely trajectory of your business over the next three to five years.

Understanding the cost of capital is important. The cost of debt is usually easy to know as it is stated. However, truly understanding the cost of your equity capital is not necessarily simple, especially in a growing business. The capital structure you have selected will impact the cost of your equity. Generally, a business with debt has a higher cost of equity than a business with no debt. The key is understanding the impact, and finding the sweet spot in the debt and equity mix.

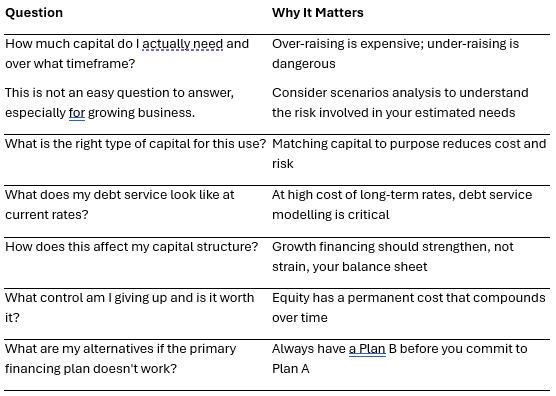

The Growth Financing Checklist

Before committing to a major growth initiative, work through these questions:

The Bottom Line

Growth is the right ambition. Funded carelessly, it can destroy the very value it was supposed to create.

In a high-rate environment, the businesses that grow successfully are the ones that think carefully about how they fund that growth, matching capital to purpose, managing their cost of capital actively, and building financial flexibility into the plan rather than hoping they won't need it.

Discipline, planning, and a clear-eyed understanding of what growth actually costs and what it's worth is what enables business to scale efficiently.

We help SME leaders plan and execute growth financing from capital structure advice and financial modelling through to debt advisory and transaction support. If growth is on your agenda, we'd be glad to be part of the conversation. Contact us!