How to Know If Your Business Is Actually Healthy: The Numbers That Matter

Most business owners have a feeling about how their business is doing.

Revenue is up. The team is busy. Customers seem happy. Things feel good.

But feelings are not financials. And some of the most serious problems in a growing business build quietly in the background, invisible to anyone who isn't looking at the right numbers.

This post is about the numbers that actually tell you whether your business is healthy. Not the ones your accountant uses for your year-end filing. The ones that tell you, right now, whether your business is on solid ground.

Why Revenue Is Not the Answer

The first thing most business owners look at is revenue. It's the most visible number, the easiest to track, and the one that feels most like a scorecard.

The problem is that revenue tells you very little about the health of your business on its own.

A business can be growing revenue and losing money. It can be profitable on paper and running out of cash. It can be winning new customers and quietly losing its best ones. Revenue is the headline. The numbers below it tell the real story.

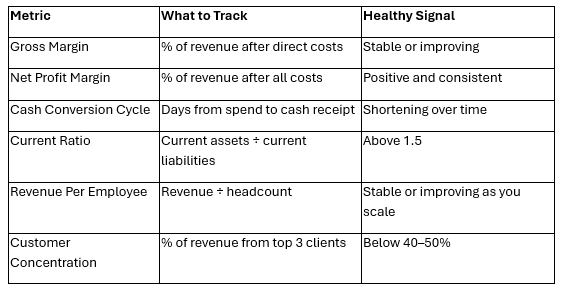

The Six Numbers That Actually Matter

1. Gross Margin

Gross margin is the percentage of revenue left after you subtract the direct costs of delivering your product or service. It's the first and most important indicator of whether your business model is fundamentally sound.

How to calculate it: (Revenue − Cost of Goods Sold) ÷ Revenue × 100

A healthy gross margin varies by industry — a software business might run at 70–80%, a manufacturing business at 30–40%, a services business somewhere in between. What matters is knowing your number, knowing what's normal for your industry, and tracking whether it's improving or deteriorating over time.

If your gross margin is shrinking, something is most likely wrong. Either your prices are too low, your costs are rising, or your mix of work is shifting toward less profitable activity. Any of these is worth understanding and addressing early.

Note on Cost of Goods Sold (COGS): It is not always straightforward to figure out the COGS. Some COGS may be fixed, some COGS need to be allocated from general expenses. The first step is to make sure you have a handle on your correct COGS.

2. Net Profit Margin

Net profit margin is what's left after all costs — including overhead, salaries, finance costs, and everything else — are deducted from revenue. It's the clearest single indicator of whether your business is genuinely profitable.

How to calculate it: Net Profit ÷ Revenue × 100

A lot of business owners are surprised when they calculate this properly for the first time. The gap between gross margin and net margin (the overhead burden) is often larger than expected, and it tends to grow as businesses scale if it isn't actively managed.

3. Cash Conversion Cycle

This is the number that catches growing businesses off guard more than any other.

The cash conversion cycle measures how long it takes for money spent running your business to come back as cash in the bank. It captures three things: how long you hold inventory before selling it, how long customers take to pay you, and how long you take to pay your suppliers.

Why it matters: A business can be profitable and cash-flow-negative at the same time if, for example, customers pay slowly, inventory sits too long, or suppliers demand payment faster than cash comes in. This is one of the most common causes of cash crises in growing businesses, and it's entirely invisible if you're only looking at your profit and loss statement.

A shorter cash conversion cycle means your business turns activity into cash quickly. A longer one means you need more working capital to fund the gap and the faster you grow, the more capital that gap consumes.

4. Current Ratio

The current ratio measures your short-term financial resilience: whether your business has enough liquid assets to cover its short-term obligations.

How to calculate it: Current Assets ÷ Current Liabilities

A ratio above 1.5 generally indicates a healthy liquidity position. Below 1.0 means your current liabilities exceed your current assets, a warning sign that deserves immediate attention.

Banks look at this number. Investors look at it. And it's one of the earliest indicators of financial stress. A business that is profitable but has a deteriorating current ratio is building up a problem that will eventually surface as a cash flow crisis.

5. Revenue Per Employee

Revenue per employee is a simple but powerful indicator of operational efficiency: how productively your business is converting its headcount into revenue.

How to calculate it: Total Revenue ÷ Number of Employees

This number varies enormously by industry, but the trend matters as much as the absolute figure. If revenue per employee is declining as you grow, it means your costs are scaling faster than your output, a warning sign that your operating model needs attention before it becomes a profitability problem.

6. Customer Concentration

This one doesn't show up in your financial statements at all but it's one of the most significant risk factors in a growing business.

Customer concentration measures how dependent your revenue is on a small number of clients. If your top three customers represent 60% or more of your revenue, your business is significantly exposed. Losing one of them is not just a revenue problem, it's potentially an existential one.

Healthy businesses actively manage concentration risk by growing the customer base, by developing recurring revenue streams, and by understanding which client relationships are most at risk at any given time.

7. Other Key Performance Indicators (KPIs)

There are many other KPIs that may be relevant to your business. Quick examples include Client Acquisition Cost, Lifetime Value, Open projects at any given time, and many more. The key with KPIs is to find the one that matters to your business and begin tracking them to make sure you have a 360 view of your business.

How to Use These Numbers

Knowing these six numbers is the starting point. Using them is what creates value.

The businesses that manage their financial health well don't just calculate these numbers once a year. They track them monthly, building a simple dashboard that shows where each metric stands, how it's trending, and where it's moving outside of a healthy range.

That monthly rhythm creates something that most small business owners don't have: early warning. Problems that would otherwise surface as a cash crisis or a sudden profitability decline become visible weeks or months earlier when there's still time to do something about them.

A Simple Financial Health Dashboard

The Honest Question

Here's the question worth sitting with: if someone asked you right now what your gross margin is, what your current ratio is, and what percentage of your revenue comes from your top three clients, could you answer without looking it up?

If the answer is no, you don't have visibility over your business's financial health. You have a feeling about it which is a very different thing.

The good news is that getting visibility isn't complicated. It requires the right metrics, tracked consistently, by someone who knows what to look for. That's exactly what a proper finance function, whether internal or fractional, is designed to provide.

Also, think about this as continuous improvement. You have been tracking revenues since inception, so now adding Gross Margin and Net Profit Margin would likely be relatively easy. Then, add another metric and another one. Make sure you don’t make your monthly processes overly complex but get the information you need to make sure you can run your business properly.

The Bottom Line

Revenue is not health. Busyness is not health. Growth is not health.

Financial health is about margins, cash flow, liquidity, efficiency, and resilience, measured consistently and acted on early.

The businesses that build long-term value are the ones that know their numbers. Not just the headline, but the story underneath it.

We help growing businesses build the financial visibility to understand and improve their financial health. If you're not confident you're looking at the right numbers, we'd be glad to have that conversation. Book a call here