What to Do Before You Talk to Your Bank. How to Walk Into That Conversation Prepared

In the current rates environment where rates aren't falling, credit conditions remain selective, and banks are more cautious than they were two years ago, the businesses that access financing successfully are the ones that walk into those conversations prepared.

This post is about how to do that.

Why Bank Conversations Go Wrong

Most business owners approach their bank the wrong way.

They arrive with a number (and even then, sometimes they don’t even have the figure): how much they need and a rough idea of what it's for. They expect the bank to figure out the rest. And when the answer comes back slower than expected, more conditional than anticipated, or simply no, they're surprised.

Banks are not adversaries. But they are analytical institutions with specific criteria, risk frameworks, and internal approval processes. The businesses that get the best outcomes from their banking relationships are the ones that understand this and prepare accordingly.

Walking into a bank conversation unprepared is one of the most common and costly mistakes growing businesses make. Not because the business isn't creditworthy, but because it hasn't presented itself credibly.

What Banks Are Actually Looking For

Before you prepare anything, it helps to understand what a bank's credit team is trying to answer when they assess your request.

At its core, a bank is asking four questions:

1. Can this business repay the debt? This is about cash flow specifically, whether your business generates enough free cash flow to service the debt comfortably, with headroom. Banks want to see this demonstrated historically and projected forward. This is probably one of the biggest misconceptions with bank lending in that thinking banks will finance future cash flow. There are specialized institutions who can do this (we discussed private credit in another post), but banks are not one of them.

2. What happens if things go wrong? Banks think in downside scenarios. What's the collateral? What happens to the business if revenue drops 20%? Is there a personal guarantee? The strength of your downside case matters as much as your upside story. (We also do not like personal guarantees for small and medium business owners as it entirely destroyed the added advantage of the corporation via a separation of liability, but alas, the personal guarantee is usually not optional).

3. Does management know what they're doing? Banks back people as much as businesses. Your credibility such as your track record, your understanding of your own financials, your clarity about the plan is assessed throughout the conversation, not just in the formal application. A well-told story lands better with a bank.

4. Is this the right structure for the ask? A term loan, a revolving credit facility, an equipment finance line, different needs require different structures. A bank that sees a mismatch between what you're asking for and what you actually need will either push back or offer something that doesn't quite fit.

Understanding these four questions before you walk in lets you structure your preparation around what actually matters. And understanding how the bank thinks is also important.

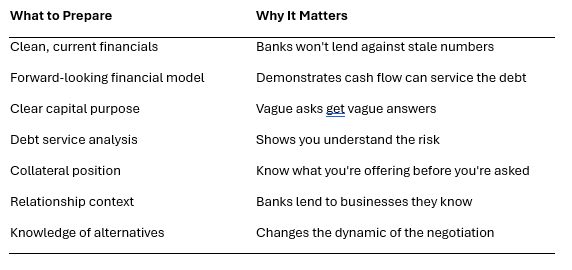

The Seven Things to Have Ready

1. Clean, current financials

This sounds obvious but is consistently where businesses fall short. Your financials need to be up to date, not last year's numbers, not draft accounts, not something your bookkeeper is still tidying up. A bank reviewing a financing request in May 2026 wants to see recent performance, not a picture from eighteen months ago.

Current means: your most recent year-end financial statements and management accounts for the current year to date.

2. A forward-looking financial model

Historical financials tell the bank where you've been. A financial model tells them where you're going and whether the debt can be serviced from projected cash flows.

Your model doesn't need to be complex. It needs to be credible. Month-by-month revenue and cost projections, a clear cash flow forecast, and a debt service coverage calculation that shows the bank you've thought through how repayment works.

In the current rate environment with no cuts on the horizon and borrowing costs remaining elevated, your debt service coverage needs to be robust. Banks are stress-testing more carefully than they were two years ago.

3. A clear purpose for the capital

"We need working capital" is not a clear purpose. "We need a $2M revolving credit facility to support a 45-day receivables cycle as we scale from $8M to $12M in revenue over the next 18 months" is a clear purpose.

The more specific you are about what the money is for, why you need it now, and how it connects to your business plan, the more credible your request becomes.

4. A debt service analysis

Show the bank, before they ask, that you've modelled the repayment. What does the monthly or quarterly debt service look like? What's your coverage ratio at current performance? What's the coverage ratio if revenue comes in 15% below plan?

This single piece of analysis does more to build credibility with a bank than almost anything else. It signals that you understand the risk and have thought through the numbers.

5. Your collateral position

Know what you're offering before you're asked. Real estate, equipment, receivables, inventory: what assets does your business have that could secure the lending? And what's already charged against them?

If you're going into a conversation without a clear picture of your collateral position, you're negotiating blind.

6. A relationship context

Banks lend to businesses they understand. If this is your first significant financing conversation with your bank, consider whether there's groundwork to lay first: a meeting to update them on the business, a conversation about your growth plans, a chance to build the relationship before you need something from it.

The businesses that get the best terms from their banks are almost never the ones that only call when they need money.

7. An understanding of the alternatives

Walking into a bank conversation knowing that private credit, mezzanine financing, or other capital sources are available to you changes the dynamic of the negotiation. You're not a supplicant; you're a business with options choosing the best one.

That posture, calm, informed, not desperate, comes through in the conversation. And it produces better outcomes.

8. If you are in trouble, your bank will likely not be interested

This is something we see a lot. Businesses who find themselves in a difficult position think they can just talk to the bank and get a lifeline. If you are struggling, it is already too late and your bank will know. Put the line of credit in place early, when the business is strong.

If you foresee difficulties ahead, discuss with your bank before the storm emerges, you will have a much better chance of gaining their support.

A Note on Timing

First, start earlier than you think you need to. A bank process that takes eight to twelve weeks in a benign environment can take longer when conditions are tighter. If you need capital by a certain date, work backwards from that date and start preparing now.

Second, make sure your financial story is as strong as it can be before you go in. This is not the environment to walk into a bank conversation with rough numbers and a general idea. The businesses getting financing in 2026 are the ones with clean financials, credible projections, and a clear ask.

What Good Preparation Looks Like

The Bottom Line

A bank conversation is not a pitch. It's an assessment. And the businesses that perform best in that assessment are the ones that have done the work before they walk in the door.

In the current rate environment, with capital more selective and banks more cautious, preparation is not optional. It's the difference between a yes and a no or between good terms and terms you'll be living with for years.

If a financing conversation is on your horizon, start the preparation now. The businesses that access capital on the best terms are the ones that made themselves easy to say yes to.

We help SME leaders prepare for and navigate banking and financing conversations — from building the financial model to structuring the ask and managing the process. If a capital raise is on your agenda, we'd be glad to have that conversation first. Book a call here