Private Credit Is No Longer a Last Resort — Here's What SME Leaders Need to Know

For a long time, private credit had a reputation problem.

If your bank said no, you went to a private lender. Higher rates, tighter terms, and a quiet admission that your business couldn't get financing through the front door.

That perception is outdated and clinging to it is costing SMEs real money and real opportunity.

Private credit has fundamentally changed over the past decade. It has grown into a mature, sophisticated asset class that now sits alongside, not below, traditional bank financing. The businesses that understand this are accessing capital on better terms, with more flexibility, and faster than those still waiting in line at their bank.

This post is about what private credit actually is today, why it matters for SME leaders, and how to think about it as part of your capital strategy.

What Private Credit Actually Is

Private credit refers to lending that happens outside of public markets and traditional banks. It includes direct lending, mezzanine financing, unitranche facilities, asset-based lending, and a range of other structures.

The common thread is that the capital comes from institutional investors: pension funds, insurance companies, private equity firms, family offices, rather than from a bank's deposit base.

Because private credit lenders are not subject to the same regulatory constraints as banks, they can move faster, structure more creatively, and take on complexity that a bank's credit committee would simply decline.

That last point matters more than most business owners realise.

Why Banks Are Not Always the Right Answer

Banks are excellent at financing businesses that fit neatly into their credit boxes. Strong balance sheets, clean financials, predictable cash flows, established operating history and if you have all of that, your bank will likely give you a competitive rate and reasonable terms.

But most growing and ambitious businesses don't fit neatly into a box. They have:

Complex capital structures from acquisitions or growth financing

Seasonal or lumpy cash flows that look concerning on a standard credit model

Significant intangible assets that don't show up well on a balance sheet

A temporary period of underperformance following an investment cycle

A transaction like a buy, a sell, a recapitalisation that requires speed and certainty

In all of these situations, a bank's answer is often slow, partial, or no. Not because the business isn't creditworthy but because it doesn't fit the model.

Private credit lenders are built for exactly these situations.

The Three Things Private Credit Does Better Than a Bank

1. Speed and certainty

A private credit lender can move from term sheet to close in weeks rather than months. For businesses in a time-sensitive transaction or facing a financing gap that needs to be closed quickly, that speed is worth a significant premium.

2. Structural flexibility

Private credit lenders can build financing solutions that a bank simply cannot offer. Covenant-lite structures, PIK interest options, deferred amortisation, equity co-investment. These tools allow a lender to match the financing to the actual shape of the business rather than forcing the business to conform to a standard product.

3. Relationship-based underwriting

Private credit lenders underwrite businesses, not just financials. They will take the time to understand your business model, your management team, your market position, and your trajectory. A business with a compelling story and a temporary blemish on its financials has a far better chance with a private credit lender than with a bank credit committee reviewing a spreadsheet.

What It Costs And Why the Math Often Works

The honest answer is that private credit is more expensive than bank debt. Rates are typically higher, and there are often arrangement fees and other costs built into the structure.

But the comparison is rarely as simple as rate A versus rate B.

The right question is: what is the cost of not having the capital?

For a business pursuing an acquisition, a missed deal is not a zero-cost outcome. For a business navigating a temporary cash flow challenge, a financing gap can be existential. For a business that could grow faster with the right capital structure, the opportunity cost of staying with a conservative bank facility can be enormous.

When you frame the comparison correctly — not bank rate versus private credit rate, but the full cost and benefit of each option — private credit often makes compelling sense.

The Private Credit Landscape Today

The private credit market has grown significantly over the past decade and now includes a wide range of lenders active in the SME and mid-market space globally.

At the smaller end of the market, there are boutique direct lenders focused on specific sectors or deal types. In the mid-market, large institutional platforms deploy capital directly into businesses, often with more sophistication and flexibility than any traditional bank can offer.

The range of options available to a well-advised SME is broader than most business owners realise. The challenge is knowing who the right lenders are for your specific situation, because private credit is not a commodity market with published rates and standard products. It is a relationship-driven market where access and positioning matter enormously.

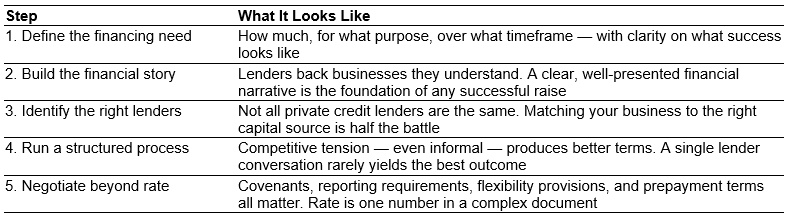

What Good Looks Like

A well-structured private credit process for an SME typically involves:

The Bottom Line

Private credit is not a last resort. For the right business, in the right situation, it is often the smartest financing decision available.

The businesses that access it well are not the ones that stumble into it after their bank says no. They are the ones that understand the full landscape of capital options available to them and have the advisors and relationships to navigate it effectively.

If your business is growing, transacting, or facing a situation that your bank can't finance cleanly. private credit is worth understanding properly.

Navigating the private credit market requires relationships and expertise. We work with SMEs to access the right capital at the right terms through our proprietary network and our own capital. Book a call to find out more