Are You Pricing Your Product or Service for Profit or Just for Survival?

Most business owners set their prices once when they launch and then quietly avoid revisiting them.

It's understandable. Pricing feels risky. Raise your prices and you might lose customers. Keep them where they are and at least the phone keeps ringing.

But here's the problem with that logic: staying busy and being profitable are not the same thing. And a pricing strategy built on fear — or on what competitors charge, or on what "feels right" is one of the most common reasons growing businesses stay stuck.

This post is about how to think about pricing properly, why most small business owners are leaving money on the table, and what to do about it.

The Most Common Pricing Mistake

The most common way small businesses set prices is cost-plus pricing: figure out what something costs to deliver, add a margin, and call it a price.

It sounds logical. The problem is that most business owners dramatically underestimate their true costs particularly indirect ones.

When you price a product or service, your costs include more than the obvious ones. They include:

Your time (often the most underpriced input of all)

Overhead: rent, software, insurance, admin

The cost of slow-paying customers and late invoices

Errors, rework, and warranty costs

The cost of sales: the time spent winning the work that didn't convert

When you add all of that up, many businesses discover their real margin is a fraction of what they thought. Some discover they are losing money on certain products or clients entirely.

Are You Actually Profitable Or Just Busy?

Here's a simple test. For your three most common products or services, can you answer these questions without guessing?

1. What does it actually cost to deliver this, fully loaded, including your time?

2. What margin am I making after all costs?

3. If I got 50% more of this work tomorrow, would I make more money or just work harder for the same result?

If you can't answer those questions confidently, you don't have a pricing strategy. You have a pricing habit.

The Three Pricing Traps

Trap 1: Pricing against competitors instead of against value

Checking what competitors charge is useful market intelligence. Building your price around it is a mistake. You don't know their cost structure, their margins, or their strategy. Pricing yourself relative to a competitor you don't fully understand is not a strategy it's a guess dressed up as research.

Trap 2: Discounting to win work

Discounting feels like a short-term fix but creates long-term problems. It trains customers to expect lower prices. It attracts price-sensitive clients who leave the moment someone cheaper comes along. And it quietly erodes the margin that keeps your business healthy.

The businesses that discount most are almost always the ones with the least financial visibility they don't know their true margins, so they don't know how much they're giving away.

Trap 3: Not raising prices when costs rise

Input costs go up every year. Labour, materials, software, insurance — all of it trends upward. If your prices stay flat while your costs increase, your margins compress slowly and silently. Most business owners don't notice until it's already a problem.

A simple rule: review your pricing at least once a year. Build price increases into your business rhythm the same way you build in budget reviews.

What Good Pricing Looks Like

Pricing done well is not about charging as much as the market will bear. It's about understanding what your work is genuinely worth, pricing to reflect that, and being confident enough to hold the line.

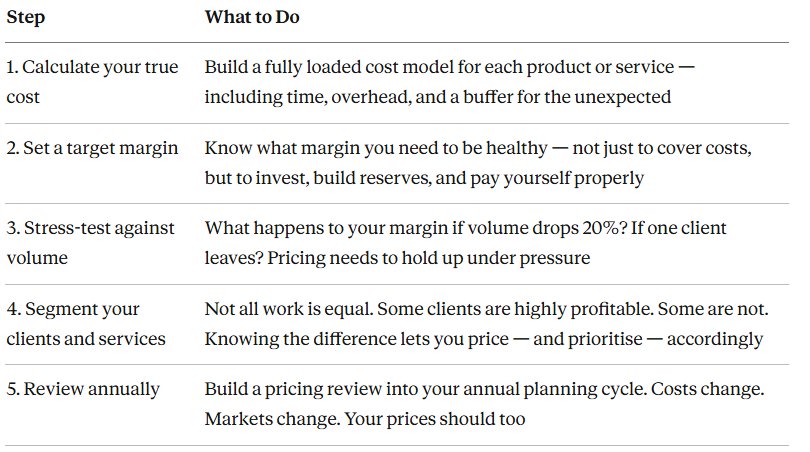

Here's a framework that works for most small and growing businesses:

The Confidence Problem

Here's something worth naming directly: a lot of pricing problems are not financial problems. They're confidence problems.

Many business owners charge less than they should because they're worried customers won't pay more, or because they feel uncomfortable defending a higher price, or because they've never actually tested the ceiling.

The businesses that price well are almost always the ones that can articulate clearly what they deliver and why it's worth what they charge. That clarity about your value proposition, your differentiation, your outcomes for clients is the foundation that good pricing is built on.

If you're not sure your pricing reflects the value you deliver, that's worth exploring. Not just as a finance exercise, but as a business strategy conversation.

What This Looks Like in Practice

A good financial function whether that's an internal finance team, a fractional CFO, or a proper advisory relationship should be able to tell you:

Which of your products or services are most profitable, and which are least

Where your pricing is strong and where it's leaving money on the table

How your margins compare to what's healthy for a business of your type and size

What a 5%, 10%, or 15% price increase would mean for your bottom line in real numbers

Most small business owners have never had that conversation. They're running on instinct and habit rather than data and strategy.

That's the gap good financial support closes.

The Bottom Line

Pricing is not a set-and-forget decision. It's one of the highest-leverage levers in your business and one of the most neglected.

A 5% price increase, applied consistently, does more for your profitability than almost any cost-cutting exercise you could undertake. But most businesses never get there because they're too busy surviving to step back and think strategically about what they charge.

If you're not confident that your pricing reflects your true costs, your value, and a healthy margin that's worth fixing. The businesses that get this right are the ones that grow sustainably rather than just staying busy.

Wondering whether your pricing strategy is working as hard as it should? We help growing businesses build the financial clarity to make decisions like this with confidence.